图书简介

These papers discuss how to invest assets over time to achieve satisfactory returns subject to uncertainties, various constraints and liability commitments. They integrate a number of techniques and discuss various models that may lead to future novel applications, i.e. financial engineering.

馆藏图书馆

Harvard Library

Princeton University Library

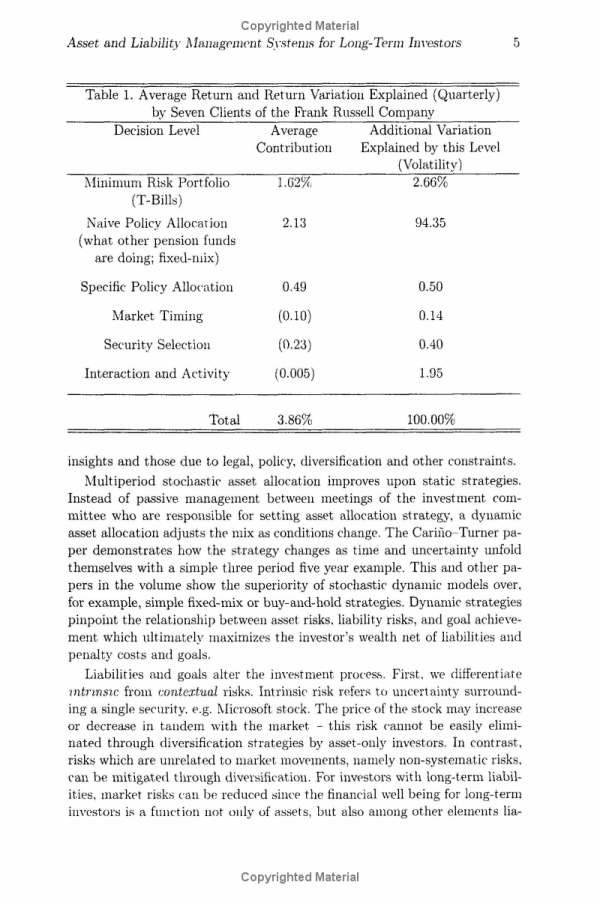

Part I. Introduction: 1. Asset and liability management systems for long-term investors: discussion of the issues John M. Mulvey and William T. Ziemba; Part II. Static Portfolio Analysis for Asset Allocation: 2. The importance of the asset allocation decision Chris R. Hensel, D. Don Ezra and John H. Ikliw; 3. The effect of errors in means, variances, and covariances on optimal portfolio choice Vijay K. Chopra and William T. Ziemba; 4. Making superior asset allocation decisions: a practitioner’s guide Chris R. Hensel and Andrew L. Turner; Part III. Performance Measurement Models: 5. Attribution of performance and holdings Richard C. Grinold and Kelly A. Easton; 6. National versus global influences on equity returns Stan Beckers, Gregory Connor and Ross Curds; 7. A global stock and bond model Lucie Chaumeton, Gregory Connor and Ross Curds; Part IV. Dynamic Portfolio Models for Asset Allocation: 8. On timing the market: the empirical probability assessment approach with an inflation adapter Robert R. Grauer and Nils Hakansson; 9. Multiperiod asset allocation with derivative assets David R. Carino and Andrew L. Turner; 10. The use of Treasury bill futures in strategic asset allocation programs Michael J. Brennan and Edwardo S. Schwartz; Part V. Scenario Generation Procedures: 11. Barycentric approximation of stochastic interest rate processes Karl Frauendorfer and Michael Schürle; 12. Postoptimality for scenario based financial planning models with an application to bond portfolio management Jitka Dupacova, Marida Bertocchi and Vittorio Moriggia; 13. The Towers Perrin global capital market scenario generation system John M. Mulvey and A. Eric Thorlacius; Part VI. Currency Hedging and Modelling Techniques: 14. An algorithm for international portfolio selection and optimal currency hedging Markus Rudolf and Heinz Zimmerman; 15. Optimal insurance asset allocation in a multi-currency environment John C. Sweeney, Steve Sonlin, Salvatore Correnti and Amy P. Williams; Part VII. Dynamic Portfolio Analysis with Assets and Liabilities: 16. Optimal investment strategies for university endowment funds Robert C. Merton; 17. Optimal consumption-investment decisions allowing for bankruptcy: a survey Suresh Sethi; 18. Solving stochastic programming models for asset/liability management using iterative disaggregation Pieter Klaassen; 19. The CALM stochastic programming model for dynamic asset-liability management Georgio Consigli and Michael A. H. Dempster; 20. A dynamic model for asset liability management for defined benefit pension funds Cees Dert; 21. Asset and liability management under uncertainty for fixed income securities Stavros A. Zenios; Part VIII. Case Studies of Implemented Asset-liability Management Models: 22. Modelling and management of assets and liabilities of pension plans in The Netherlands Guus C. E. Boender, Paul van Aalst and Fred Heemskerk; 23. Integrated asset-liability management: an implementation case study Martin Holmer; Part IV. Total Integrated Risk Management Models: 24. The Russell-Yasuda Kasai model: an asset/liability model for a Japanese insurance company using multistage stochastic programming David R. Carino, Terry Kent, David H. Myers, Celine Stacy, Michael Sylvanus, Andrew Turner, Kanji Watanabe and William T. Ziemba; 25. The home account advisor: asset and liability management for individual investors Adam J. Berger and John M. Mulvey.

Trade Policy 买家须知

- 关于产品:

- ● 正版保障:本网站隶属于中国国际图书贸易集团公司,确保所有图书都是100%正版。

- ● 环保纸张:进口图书大多使用的都是环保轻型张,颜色偏黄,重量比较轻。

- ● 毛边版:即书翻页的地方,故意做成了参差不齐的样子,一般为精装版,更具收藏价值。

关于退换货:- 由于预订产品的特殊性,采购订单正式发订后,买方不得无故取消全部或部分产品的订购。

- 由于进口图书的特殊性,发生以下情况的,请直接拒收货物,由快递返回:

- ● 外包装破损/发错货/少发货/图书外观破损/图书配件不全(例如:光盘等)

并请在工作日通过电话400-008-1110联系我们。

- 签收后,如发生以下情况,请在签收后的5个工作日内联系客服办理退换货:

- ● 缺页/错页/错印/脱线

关于发货时间:- 一般情况下:

- ●【现货】 下单后48小时内由北京(库房)发出快递。

- ●【预订】【预售】下单后国外发货,到货时间预计5-8周左右,店铺默认中通快递,如需顺丰快递邮费到付。

- ● 需要开具发票的客户,发货时间可能在上述基础上再延后1-2个工作日(紧急发票需求,请联系010-68433105/3213);

- ● 如遇其他特殊原因,对发货时间有影响的,我们会第一时间在网站公告,敬请留意。

关于到货时间:- 由于进口图书入境入库后,都是委托第三方快递发货,所以我们只能保证在规定时间内发出,但无法为您保证确切的到货时间。

- ● 主要城市一般2-4天

- ● 偏远地区一般4-7天

关于接听咨询电话的时间:- 010-68433105/3213正常接听咨询电话的时间为:周一至周五上午8:30~下午5:00,周六、日及法定节假日休息,将无法接听来电,敬请谅解。

- 其它时间您也可以通过邮件联系我们:customer@readgo.cn,工作日会优先处理。

关于快递:- ● 已付款订单:主要由中通、宅急送负责派送,订单进度查询请拨打010-68433105/3213。

本书暂无推荐

本书暂无推荐